What is a Secured Loan?

A Secured Loan (or homeowner loan) lets you borrow more by using your property as security. This can help you access better rates, even if your credit score isn’t perfect. You may also be approved to borrow a larger amount of money than with an Unsecured Loan.

What can I use a Secured Loan for?

If you’re looking to consolidate some debt, make home improvements, or fund a big purchase, a Secured Homeowner Loan is a great option to consider. Interest rates are usually lower than an unsecured personal loan as there is more security for the lender.

- Consolidating existing debts

- Making home improvements

- Both of the above, and other large expenses

Helps to reduce your monthly outgoings

Credit cards, loans and other credit commitments could be consolidated into one affordable monthly repayment, potentially saving you £100's every month.

- Lower monthly payments

- Consolidate credit cards and loans

- Average reduction in outgoings of over £600 per month for customers taking a debt consolidation loan in the last 12 months

We’ve partnered with Fluent Money to find you a great deal

Our specialist loans partner Fluent Money will help you find the right Secured Loan to suit your needs.

Important Notice: Fees may be payable on depending on your choice of financial product. This will depend on your circumstances and will be discussed at the earliest opportunity. Think carefully before securing other debts against your home. Your home may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it. If you are thinking of consolidating existing borrowing you should be aware that you may be extending the terms of the debt and increasing the total amount you repay.

How much can I borrow with a Secured Loan?

Secured Loans range from £10,000 to £500,000. How much you can borrow will depend on the lender’s criteria, your credit history, house value and equity in your property i.e., the portion you own outright.

Secured Loans: What you need to know before you borrow

When considering a Secured Loan, it’s important to understand both the benefits and risks so you can make the right choice for your situation.

Why choose a Secured Loan?

- Lower Interest Rates – Typically cheaper than Unsecured Loans, helping you save on borrowing costs.

- Borrow More – Get access to larger loan amounts, from £10,000 to £500,000.

- Flexible Repayment Terms – Choose a term that works for you, from 1 to 30 years.

- Bad Credit? No Problem – More options are available even if your credit score isn’t perfect.

Things to consider:

- Your Home Secures the Loan – Because your property is used as security, it’s important to ensure repayments fit within your budget.

- Long-Term Costs – A longer loan term can lower monthly payments but may mean paying more interest over time.

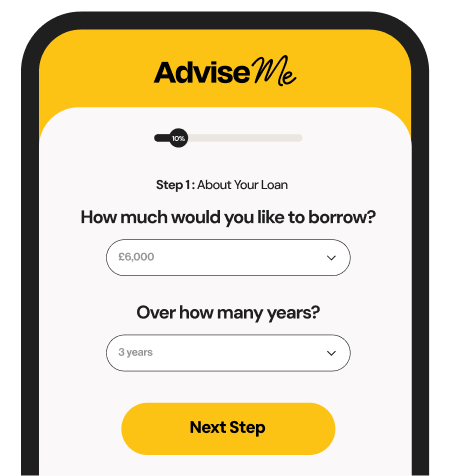

3 Easy Steps to Your Perfect Secured Loan

Get personalised deals and find the right homeowner loan for you.

Answer a few quick questions to see if you qualify—without affecting your credit score.

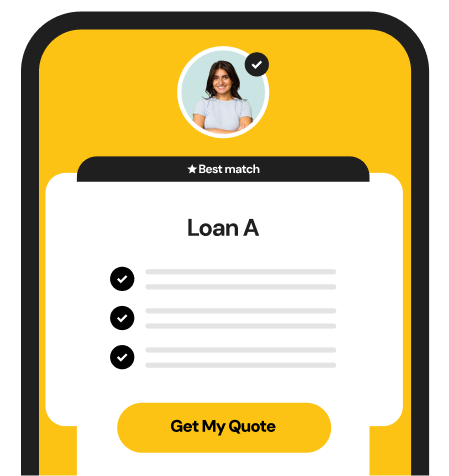

A dedicated adviser will handle the paperwork and secure the best deal for you.

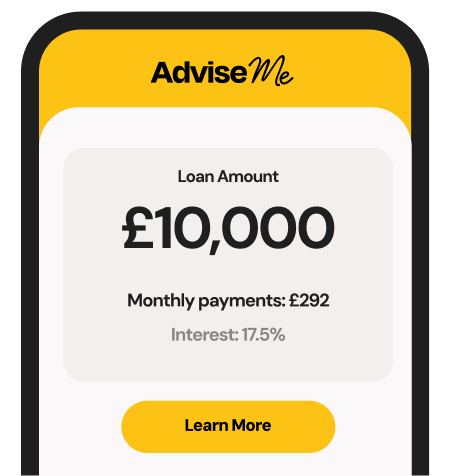

Once approved, your loan is transferred—often within two weeks.

Frequently Asked Questions

A Secured Loan is a type of borrowing where you use an asset, such as your home or car, as collateral to secure the loan. This reduces the risk for lenders, which often means you can access larger amounts of money at a lower interest rate compared to unsecured Loans.

When you take out a Secured Loan, you pledge an asset as security for the loan. If you're unable to repay the loan, the lender has the right to take possession of the asset to recover the outstanding debt. However, as long as you keep up with your repayments, you'll continue to own your asset.

The key difference is collateral. A Secured Loan requires you to put up an asset, like your home, to secure the loan, while an Unsecured Loan doesn’t. As a result, Unsecured Loans tend to have higher interest rates and are available for smaller amounts compared to Secured Loans.

Eligibility for a Secured Loan typically depends on a few key factors:

- The Asset – You’ll need to have an asset, such as a property or vehicle, that you can use as collateral to secure the loan. The value of the asset will influence how much you can borrow.

- Your Financial Situation – Lenders will assess your ability to repay the loan, including your income, existing debts, and monthly expenses. They want to ensure you can afford the repayments.

- Your Credit History – While a Secured Loan is more flexible for those with less-than-perfect credit, lenders may still look at your credit score to determine the interest rate and loan terms.

- Age and Residency – You typically need to be over 21 and a resident in the country where you’re applying for the loan.

Each lender has their own criteria, so it’s always a good idea to check with them directly to understand the specific requirements.

Yes! One of the advantages of Secured Loans is that they offer more flexibility for borrowers with less-than-perfect credit. Since the loan is backed by collateral, lenders may be more willing to approve your application, even if your credit score isn’t ideal.

The amount you can borrow depends on the value of the asset you're using as collateral, your financial situation, and the lender’s criteria. Secured Loans typically range from £10,000 to £500,000, but in some cases, borrowing up to £1 million is possible with select lenders. It's always best to check with your lender for specific limits and options available to you.

Secured Loans typically have flexible repayment terms, ranging from 1 year to 30 years, depending on the lender and the amount you're borrowing. A longer term can mean smaller monthly payments, but you may end up paying more in interest over time.

Yes, there can be fees associated with Secured Loans. These might include arrangement fees, valuation fees, or early repayment charges. It’s important to check the loan agreement carefully and ask the lender about any fees upfront, so there are no surprises later.

Yes, you can usually pay off a Secured Loan early, but some lenders may charge an early repayment fee. This is to cover the costs the lender might lose due to you repaying the loan before the agreed term. Be sure to check if any fees apply before making early payments.

A Secured Loan can affect your ability to remortgage or sell your home because the loan is tied to the property. If you want to sell, you’ll need to pay off the loan in full before transferring ownership. Similarly, if you want to remortgage, the Secured Loan may need to be cleared or included in the new mortgage arrangement.

Check Your Eligibility in Minutes

Important Notice:

Fees may be payable on depending on your choice of financial product. This will depend on your circumstances and will be discussed at the earliest opportunity.

Think carefully before securing other debts against your home. Your home may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it. If you are thinking of consolidating existing borrowing you should be aware that you may be extending the terms of the debt and increasing the total amount you repay.